Mandatory information to be included on an invoice

Updated on 31/10/2020

An invoice is evidence of a transaction. It must include all information required by law, in particular by the French Commercial Code. It is also an accounting document and is used to work out VAT duties. An invoice must therefore also show the information required by French tax law.

It is mandatory to raise invoices between professionals for any purchases of products or any provision of services. The invoice must be made in duplicate: one for the seller and one for the buyer.

However, between a company and an individual, the billing obligations depend on the transaction:

- For the sale of goods, an invoice must be issued at the customer’s request

- For distance sales, an invoice must always be issued

- For the provision of services, an invoice must be issued when the value, including tax, exceeds € 25 or at the customer’s request

This guide takes into account French Ordinance no. 2019-359 of 24 April 2019, which provides for new mandatory information on invoices.

They key information below is organised as follows:

- Mandatory information when the invoice is intended for an individual

- Mandatory information when the invoice is intended for a professional

- Specific wording to use

- The information provided for by French tax law

Information on electronic invoicing follows at the end of this article.

I – MANDATORY INFORMATION WHEN AN INVOICE IS INTENDED FOR AN INDIVIDUAL

- Invoice issue => Date the invoice is raised

- Invoice number => Unique number based on a continuous chronological sequence, without a break. It is possible to issue separate series, for example using a prefix for the year (2020-XX) or year and month (2020-01-XX). This must appear on all pages of the invoice.

- Purchase order number

- Date of sale or service => Effective date of delivery or completion of performance

- Buyer’s identity => Name and address (unless the buyer refuses to provide this)

- Billing address if different, delivery address

- Identity of the seller or service provider:

- Name and first name if an individual entrepreneur, followed by the business name if they have one

- Company name, followed by the SIREN or SIRET number

- RCS number for a merchant, followed by the city where the commercial court register is held

- Number in the Trades Directory for an artisan (SIREN + RM + number of the registration department)

- Address of the registered office (not of the branch/local office)

- If the business is a company, its legal form (E.U.R.L., S.A.R.L., S.A., S.N.C., S.A.S.) and its share capital

Please note: if the company is still being registered, the invoice must be drawn up in the name of the company and be marked “SIRET pending”.

- The seller’s individual VAT identification number, except for invoices totalling € 150 or less

- Description of the product or service => Nature, brand, reference number, etc.

- Services => Breakdown of materials supplied and labour

- Detailed account of each service and product provided

- Catalogue price(s)

- Possible price increases (shipping, packing, etc.)

- Legally applicable VAT rate(s)

- Total amount of VAT. If the transactions are subject to different VAT rates, the corresponding rate must be shown on each line

- Discounts, rebates or discounts made on the date of the sale or service, excluding discounts not listed on the invoice

- Total amount payable excluding tax (without VAT) and including all taxes (with VAT)

- The payment deadline and penalties for late payment

It must also show any discount conditions that apply if the invoice is settled before the date determined from the general conditions of sale, the penalty rate payable on the day after the payment deadline shown on the invoice, and the flat fee payable for recovery costs owed to the creditor in the event of late payment.

II – MANDATORY INFORMATION WHEN AN INVOICE IS FOR A PROFESSIONAL

Invoices for professional clients differ only slightly. These obligatory details are shown in orange:

- Invoice issue => Date the invoice is raised

- Invoice number => Unique number based on a continuous chronological sequence, without a break. It is possible to issue separate series, for example using a prefix for the year (2020-XX) or year and month (2020-01-XX). This must appear on all pages of the invoice

- Purchase order number

- Date of sale or service => Effective date of delivery or completion of performance

- Buyer’s identity => Name or company name, address of the registered office. The address shown may be a different branch of a company if it is this establishment which has a business relationship with the seller and which pays the invoice

- Billing address if different, delivery address

- Identity of the seller or service provider:

- Name and first name if an individual entrepreneur, followed by the business name if they have one

- Company name, followed by the SIREN or SIRET number

- RCS number for a merchant, followed by the city where the commercial court register is held

- Number in the Trades Directory for an artisan (SIREN + RM + number of the registration department)

- Address of the registered office (not of the local office/branch)If the business is a company, its legal form (E.U.R.L., S.A.R.L., S.A., S.N.C., S.A.S.) and its share capital

Please note: if the company is in the process of being registered, the invoice must be drawn up in the name of the company and be marked “SIRET pending”

- The seller’s individual VAT identification number, except for invoices totalling € 150 or less

- Description of the product or service => Nature, brand, reference number, etc.

- Services => Breakdown of materials supplied and labour

- Detailed account of each service and product provided

- Catalogue price(s)

- Possible price increases (shipping, packing, etc.)

- Legally applicable VAT rate(s)

- Total amount of VAT. If the transactions are subject to different VAT rates, the corresponding rate must be shown on each line

- Discounts, rebates or discounts made on the date of the sale or service, excluding discounts not listed on the invoice

- Total amount payable excluding tax (without VAT) and including all taxes (with VAT)

- Payment date or deadline:

- Date on which payment is due

- Discount conditions in the event of early payment

- If there is no discount, the invoice must be marked “Discount for early payment: none”

- It must show any late payment penalties if the invoice is not settled by the payment deadline (late penalties are payable without a reminder)

- It must state the flat compensation fee of € 40 for recovery costs in the event of late payment

Please note that for any invoice raised, whether for an individual or a professional, any company that fails to comply with these obligations is at risk of being fined:

- Fiscal fine of € 15 for every missing or incorrect detail on each invoice, capped at 1/4 of its amount

- Fine of € 75,000 for a natural person (€ 375,000 for a legal person). This fine can be doubled in the event of incorrect invoicing, convenience invoices and fictitious invoices

III – SPECIAL INFORMATION

In certain specific cases, the following information should be added:

- If the seller or service provider is a member of a management centre or an approved association => “Membre d’un centre de gestion (ou association) agréé, le règlement par chèque et carte bancaire est accepté”

- If the seller or service provider benefits from VAT exemption (e.g., auto-entrepreneur), the invoice is tax-free => “TVA non applicable, Art. 293 B du CGI”

- When it states “Autoliquidation”, this clearly indicates it is an “amount excluding tax”. If works are carried out by a construction subcontractor on behalf of a principal contractor who is subject to VAT, the subcontractor no longer declares VAT. Instead, it is the principal that declares it (self-liquidation of VAT)

- Business insurance – Contact details of the insurer or guarantor – Geographic coverage of the contract or guarantee => This information must be provided by craftspeople or micro-entrepreneurs exercising a trade, for whom professional insurance is compulsory (specifically the ten-year guarantee)

- “Eco-participation DEEE” => This information relates to sales of electronic products and furniture

- In the case of buying a recording medium => “Rémunération pour copie privée (RCP)”.

IV – INFORMATION PROVIDED FOR BY TAX LAW

The French General Tax Code also imposes certain obligations. The main ones are:

- In the event of exemption, reference must be made to the relevant provision of the French General Tax Code or to the corresponding provision of Council Directive 2006/112/EC of 28 November 2006 on the common VAT system, or to any other statement indicating that the business/transaction benefits from exemption

- When the purchaser or lessee is liable for VAT, it must be marked “Autoliquidation”

- When the purchaser or lessee issues the invoice in the name of, and on behalf of, the person subject to tax, it must be marked “Autofacturation”

- When the person subject to tax uses the special scheme for travel agencies, it must be marked “Régime particulier – Agences de voyages”

- If the regime provided for by Article 297 A of the French General Tax Code applies, it must be marked “Régime particulier – Biens d’occasion”, “Régime particulier – Objets d’art” or “Régime particulier – Objets de collection et d’antiquité” depending on the transaction

- The characteristics of the new vehicle as defined in Article 298 (III) (e) of the French General Tax Code for the products or services mentioned in II above

- Separately, the hammer price of the goods, taxes, duties, fees and any ancillary costs such as commission, packaging, transport and insurance costs requested by the organiser from the buyer, for sales at public auctions referred to in Article 289 (1) (d) of the French General Tax Code made by an organiser of public auctions acting in its own name, subject to the profit margin regime defined in Article 297 A of the same Code. This invoice must not include VAT.

V – ELECTRONIC INVOICING

For an invoice to be produced in electronic format, it must be possible to guarantee the authenticity of its origin, its legibility and the completeness of its content. To do this, the company must use one of the following methods:

- Electronic signature

- Electronic data interchange (EDI) to upload invoices

A technical solution other than the use of an electronic signature, or a paper copy, as soon as the company has implemented a check system that ensures a reliable audit trail between the invoice issued or received and the corresponding delivery of goods or services

Mandatory information for electronic invoices is the same as on paper invoices.

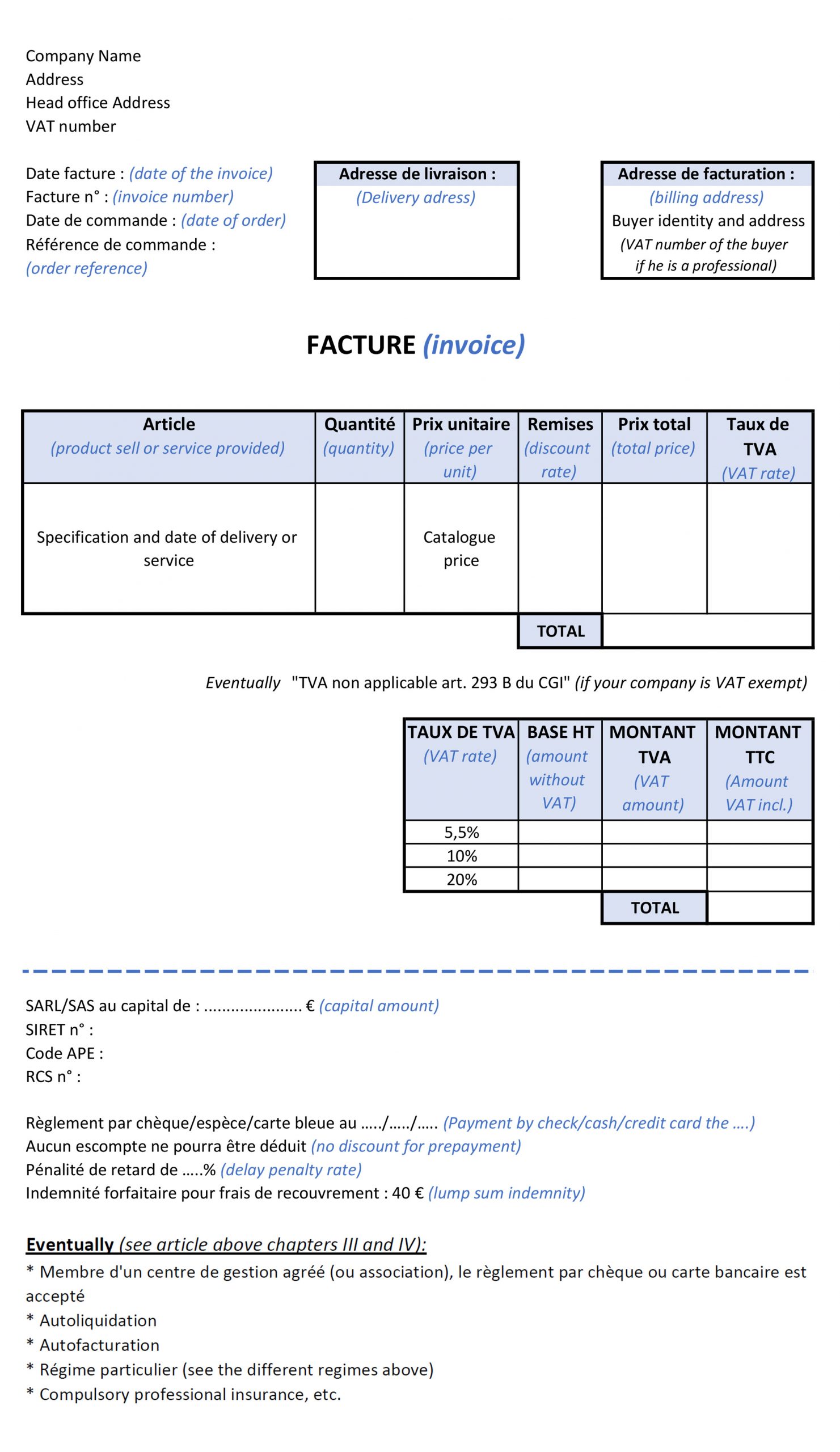

To conclude, here is an example of a standard invoice. Of course, you will need to adapt it to comply with the requirements for your own profession. Please contact us for more details.