How much money is to be paid in 2022 for professional training?

- par FBA team

As of January 1, 2022, the legal training contributions of employees must be paid to the Urssaf and the frequency of payments has changed.

This reform is accompanied by the modification of certain rules, in particular concerning the exemptions applicable to these contributions.

This concerns the CPF-CDD contribution, as well as the Cufpa (contribution to the professional training of employees, and apprenticeship tax for the main part).

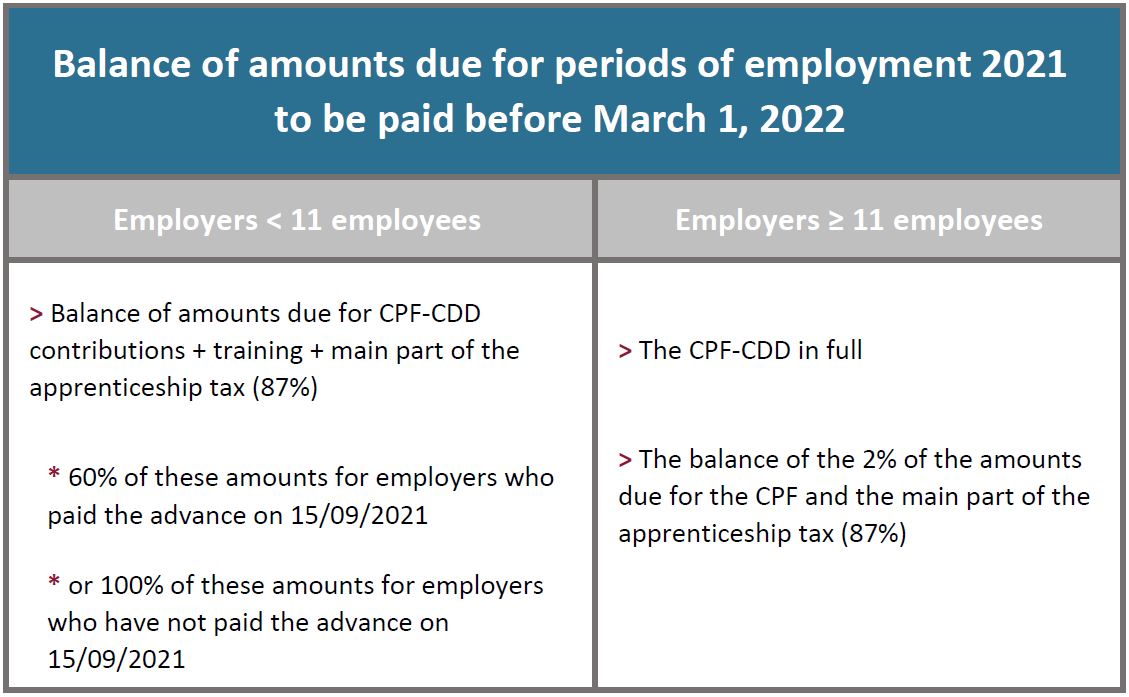

During the first quarter of 2022, employers will have to pay the balance of the sums due for the periods of employment in 2021 in addition to those due for the first months of 2022.

An intermediate balance of the apprenticeship tax has been created, calculated on the 2021 payroll. The payments must be made to the authorized training organizations before June 1st, 2022.

The balance of the apprenticeship tax calculated on the 2022 payroll will be paid to Urssaf at the time of the DSN of April 2023.

Do not hesitate to contact your payroll manager in charge of your file!

| Cookie | Durée | Description |

|---|---|---|

| cookielawinfo-checkbox-analytics | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics". |

| cookielawinfo-checkbox-functional | 11 months | The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional". |

| cookielawinfo-checkbox-necessary | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary". |

| cookielawinfo-checkbox-others | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other. |

| cookielawinfo-checkbox-performance | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance". |

| viewed_cookie_policy | 11 months | The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data. |